Global Broker Regulation Inquiry App

About WikiFX

English

简体中文

繁體中文

English

Pусский

日本語

ภาษาไทย

Tiếng Việt

Bahasa Indonesia

Español

हिन्दी

Filippiiniläinen

Français

Deutsch

Português

Türkçe

한국어

العربية

اردو

US Services Sector Surveys Signal Solid Growth In January, But...

Abstract:Following the dramatic rebound in US Manufacturing survey data - driven by a surge in new orders - '

Following the dramatic rebound in US Manufacturing survey data - driven by a surge in new orders - 'Soft' data has bounced back dramatically from its post-government shutdown lows (which is ironically occurring as the hard data - which was so resilient through the shutdown - has started to roll over)...

...and this morning's Services Sector survey data builds on that rebound

- S&P Global's US Services PMI signaled abetter than expected expansionof 52.7 in January (52.5 exp), rebounding from April 2025 lows.

- ISM's US Services PMI survey also beat expectationsin January (53.8 vs 53.5 exp), but was flat from a revised lower 53.8.

But both still solidly in expansion...

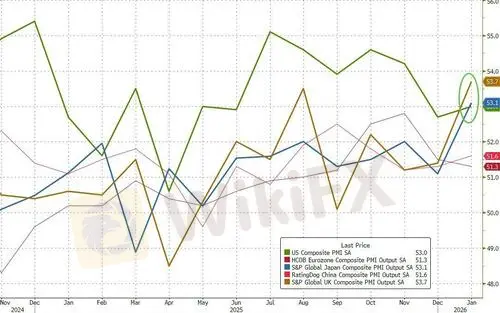

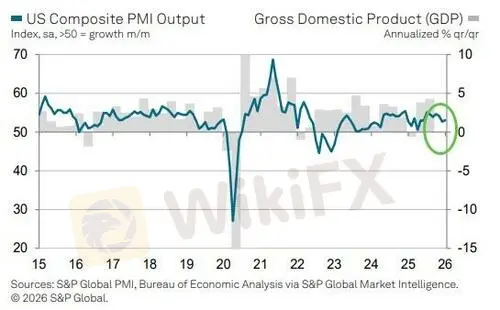

The S&P Global US Composite PMI recorded 53.0 in January. That was up from 52.7 in December and represented a solid rate of growth in private sector activity. Both sectors covered by the survey recorded stronger output expansions, in line with faster gains in new business. Employment meanwhile rose only marginally, while confidence in the outlook softened.

Despite the rebound, US has been overtaken by UK and Japan in terms of global PMIs...

according to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

However,that is a lower gear compared to the pace of expansion seen prior to Decembers slowdown, and hints at GDP growth cooling in the first quarter.

Consumer-facing companies are increasingly reporting a challenging environment, with demand for services falling in January having nearly stalled in December, “reflecting low levels of consumer sentiment and cost of living pressures,”Williamson noted.

The ISM data showed a triple whammy of higher prices, lower new orders, and lower employment...

However, as Williamson concludes, “inflationary pressures in the service sector meanwhile remain elevated, blamed on the pass though of tariff related price increases and wage growth, though stiff competition is often reported to have limited the impact on final selling prices.”

However, there is a silver lining, as Williamson concludes:

Disclaimer:

The views in this article only represent the author's personal views, and do not constitute investment advice on this platform. This platform does not guarantee the accuracy, completeness and timeliness of the information in the article, and will not be liable for any loss caused by the use of or reliance on the information in the article.

WikiFX Broker

Latest News

RoboMarkets Review: Regulation Questions Around a Broker Facing Fresh Trading Complaints

WikiFX

WikiFXReview 2026: Deriv Regulation, Complaints, and Withdrawal Risk Signals

WikiFXDSI Exposes Alleged Forex Empire Behind Billion Baht Scam, Money Laundering and Political Connection

WikiFXIUX Review:Before Investing a Single Penny, Read These Jaw-Dropping Deposit & Withdrawal Experiences

WikiFXStop Trading in the Middle of Ranging Forex Markets

WikiFXFXTF Review 2026: Regulation, Withdrawals, and Scam Allegations

WikiFXIG Review 2026: Is This Forex Broker Safe?

WikiFXsquaredfinancial Review 2026: Is This Forex Broker Safe?

WikiFXFXTF Review 2026: Japan FSA Regulation, Platform Access, and Exposure Cases

WikiFXReview 2026: FBS Regulation, Complaints, and Withdrawal Risk Signals

WikiFXCurrency Calculator

USD

CNY

Current Rate:0

Enter amount

USD

Redeemable Amount

CNY

Calculate